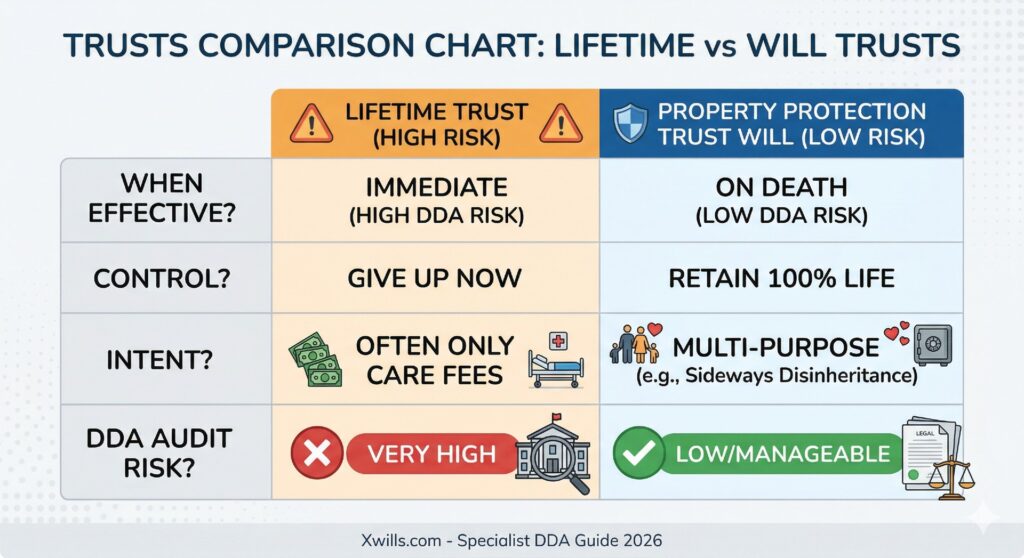

The Golden Rule: Early Intervention.

The most effective way to protect your house from care home fees is to act while you are healthy and independent. If you wait until a care need is imminent or a diagnosis is received, your planning is significantly more likely to be challenged during a local authority audit under "Deprivation of Assets" rules.

Professional planning in 2026 requires foresight. Don't leave your children's inheritance to chance. Ultimately, the best time to protect your house from care home fees is while you are healthy and independent.