Deliberate Deprivation of Assets (DDA) occurs when a local authority rules that you intentionally reduced your wealth to avoid paying care fees. In 2026, councils use the "Foreseeability Test" to decide if your planning was a legitimate family protection or a deliberate attempt to evade social care costs.

For UK homeowners, deliberate deprivation of assets occurs when you intentionally reduce your capital to avoid paying care home fees. In 2026, local authority investigations are more sophisticated than ever. This guide explains the legal boundary between "deprivation" and "legitimate estate planning."

To rule that deliberate deprivation of assets has occurred, a local authority must satisfy the "Foreseeability Test." Under 2026 Annex E guidance, they must ask: "Was it reasonable at the time of the arrangement to expect that care might imminently be required?"

To determine if a transfer is "deprivation," the Local Authority assesses two critical factors:

The council must prove that avoiding care home fees was a "significant motivation" for your actions. This is why a Property Protection Trust (PPT) Will is a robust defense—it serves multiple legal purposes beyond care fee protection:

Strategic Reality: In 2026, when estate planning serves these vital family goals, the "care fee" protection is legally viewed as an incidental benefit. This makes it nearly impossible for a council to claim deliberate deprivation, provided the Will was drafted while you were in good health.

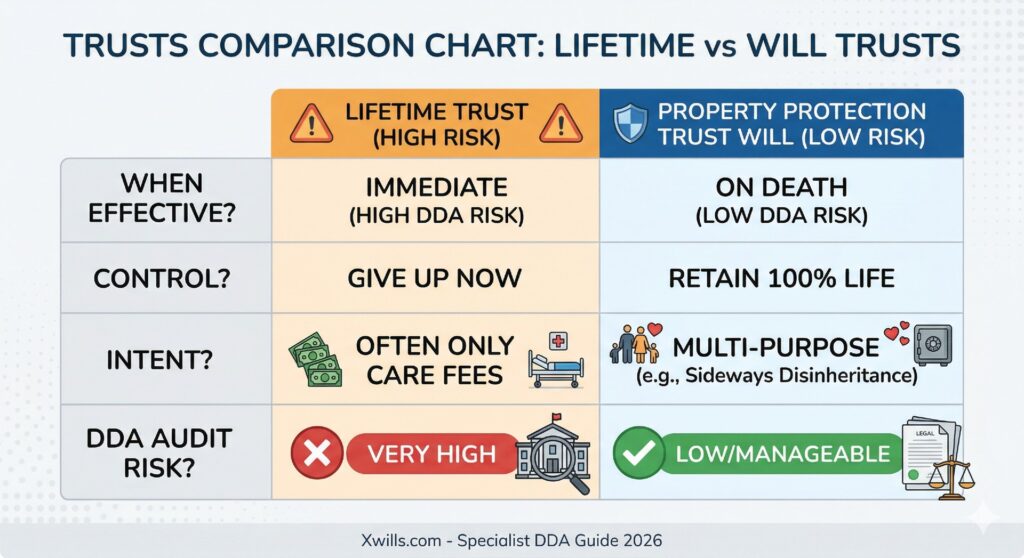

While a Property Protection Trust (PPT) in a Will is viewed as legitimate succession planning, "Lifetime Trusts" are treated with significant suspicion in 2026. Because these involve gifting your home while still living in it, they often trigger an immediate "Red Flag" for investigators.

If a council rules a Lifetime Trust as deliberate deprivation, they apply Notional Capital rules. They charge for care as if you still own the house, even though you no longer have the legal right to sell it—leaving families with massive fees and no liquid assets.

Three primary reasons Lifetime Trusts fail a 2026 audit:

The Verdict: For 90% of UK homeowners, the Property Protection Trust Will remains the "Gold Standard." It provides robust protection for the next generation without the immediate legal and tax risks of lifetime gifting.

A Property Protection Trust (PPT) created within a Will is fundamentally different from a lifetime gift. While "gifting the house" often triggers an investigation, a Will-based trust sits on firmer legal ground due to three critical factors in 2026:

Because a PPT only triggers upon the first death, you do not reduce your assets while living. You retain 100% control. Under 2026 guidelines, if you haven't reduced your capital, you cannot have "deprived" yourself of it for care fee purposes.

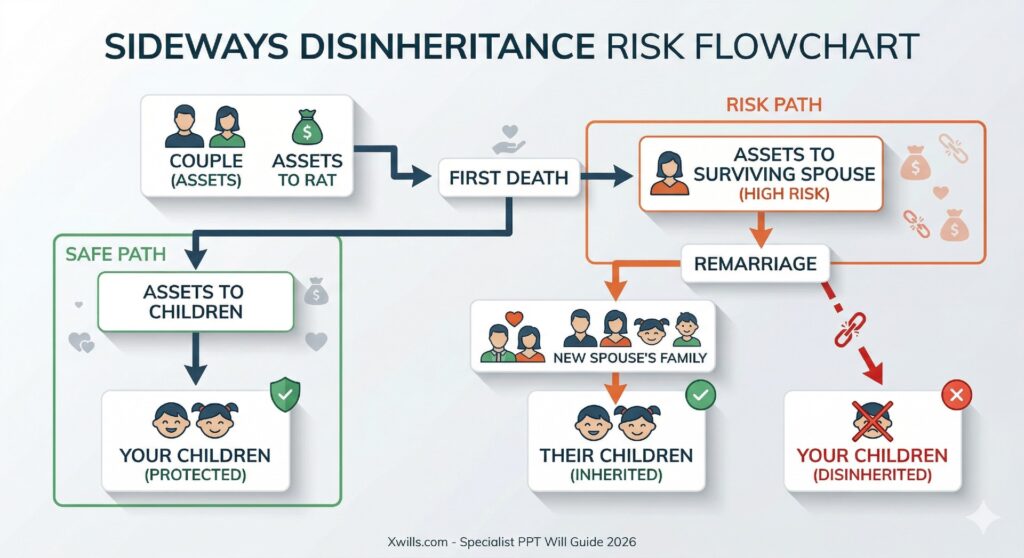

UK law protects your right to choose beneficiaries. A PPT Will is primarily used for Testamentary Freedom—protecting children from a first marriage or preventing sideways disinheritance. This broader purpose proves avoiding care fees was not the "significant motivation."

Annex E of the Care Act explicitly states councils must not automatically assume deprivation. By documenting family protection goals when the Will is made, you create a contemporary "paper trail" of legitimate intent.

Professional Insight: The Evidence Requirement

While a PPT Will is a robust strategy, it is not an "automatic shield." In 2026, local authorities look for contemporary evidence. This is why we include a professional Letter of Wishes with every PPT Will, documenting your health status and family-first intentions to pre-emptively defeat any future "Foreseeability Test."

If a local authority concludes that a deliberate deprivation of assets has occurred, they apply a complex legal mechanism known as the "Notional Capital" rule to recover care costs.

2026 Legal Alert: There is no "7-year rule" for care home fees in the UK. Local authorities can audit asset transfers from decades ago. However, under Annex E of the Care Act 2014, a PPT is a protected form of Testamentary Freedom, provided it passes the "Foreseeability Test" at the time of drafting.

The council assesses your wealth as if you still own the asset you gave away. They calculate care fees based on this "imaginary" capital, often leaving the resident with a massive weekly bill they have no liquid funds to pay.

Under the Care Act 2014, if an asset was transferred to a third party (such as a child) to avoid charges, that person can be held personally and legally liable to pay the council the difference in care costs.

The 2026 "Security Gap": Why PPTs Win

This "Clawback" risk is why "gifting the house" is a high-risk gamble. In contrast, a Property Protection Trust (PPT) Will is a secure legal framework that creates a "life interest" for the survivor without ever triggering a deprivation assessment. It protects the home without putting your children at risk of a massive legal bill.

If your total capital exceeds these limits, you are classified as a "self-funder" and must pay the full cost of care. For the official 2026 framework, refer to the DHSC Social Care Charging Circular (2026/27).

| Region | Upper Limit (Self-Funded) | Lower Limit (Full Support) |

|---|---|---|

| England & NI | £23,250 | £14,250 |

| Scotland | £35,000 | £21,500 |

| Wales | £50,000 | £50,000 (Flat Rate) |

The "Wales Exception": In Wales, a flat threshold of £50,000 applies to residential care, offering significant inherent property protection. In England, the much lower £23,250 threshold is why a Property Protection Trust (PPT) is considered the "gold standard" for homeowners.

Want the complete picture? Our DDA guide is part of our Ultimate 2026 Guide to Property Protection Trust Wills , where we break down every aspect of modern estate planning and house protection.

For the majority of UK homeowners, the Property Protection Trust (PPT) within a Will is the most robust strategy. Unlike high-risk "Lifetime Gifts," a PPT passes the 2026 local authority audit by utilizing three pillars of established UK law:

You remain the 100% legal owner of your home throughout your life. Because no asset is gifted away while you are alive, there is no "deprivation" for a council to investigate during your lifetime.

By changing from Joint Tenants to Tenants in Common, you simply define your individual 50% shares. This is standard HMRC-approved estate planning, not a "sham" transaction.

When the first spouse passes, their 50% share enters the trust. Under 2026 care funding rules, the council can only assess the survivor's 50% share, effectively shielding half the home instantly.

The 2026 Legal Intersection: A Property Protection Trust is an exercise of your Testamentary Freedom. Local Authorities assess whether the primary purpose was a legitimate desire to provide for the next generation or a significant motivation to evade care costs.

By documenting your intent to protect your bloodline from "Sideways Disinheritance" or divorce, you provide the evidence needed to show the PPT is a standard part of your succession planning, rather than a deliberate deprivation of assets.

A "one-size-fits-all" Will is a target. A specialist Property Protection Trust is a shield. Don't leave your family's future to a local authority assessment. Let our specialists review your 2026 compliance today.

Request Free 2026 Compliance Review✔ 100% Confidential & No-Obligation

0208 064 3806

info@xwills.com

Tilsop Farm,

Nash,

Ludlow,

Shropshire

SY8 3AX