Are Next of Kin Responsible for Care Home Fees?

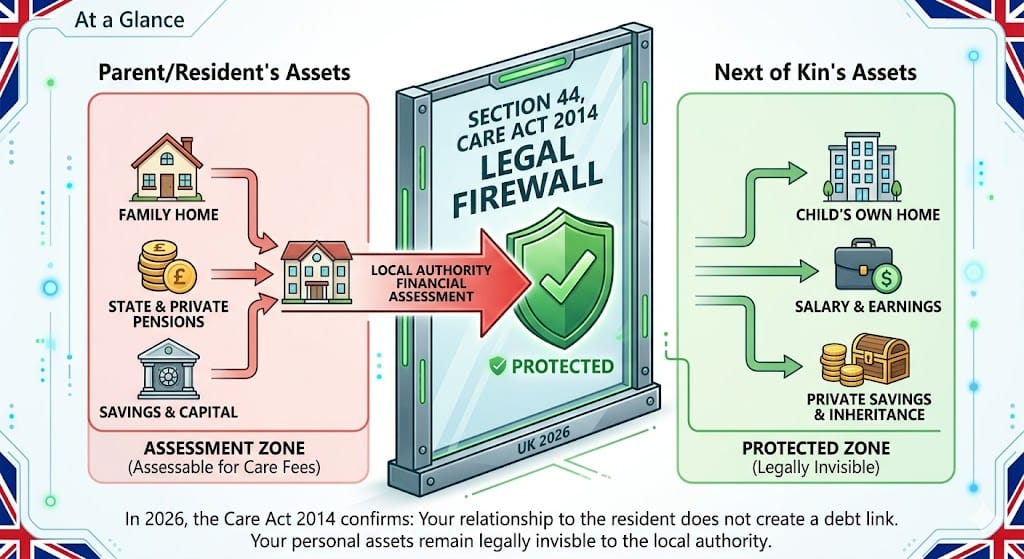

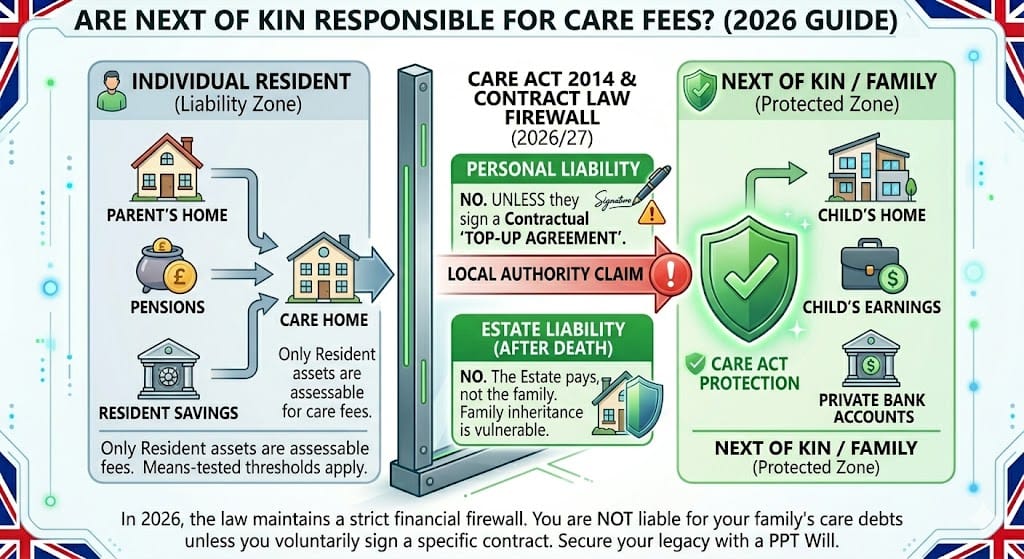

One of the most common concerns for UK families in 2026 is: Are Next of Kin Responsible for Care Home Fees? The short answer for any child, spouse, or relative is No. Under the Care Act 2014, next of kin have zero legal liability for a family member’s care costs; UK law treats every adult as a separate financial entity.

When a local authority conducts a financial assessment, they are legally restricted to looking only at the assets and income of the person receiving care. Your savings, your property, and your salary are entirely exempt from their calculations.

The 2026 Legal Reality:

Even if you are the primary "Next of Kin" or hold Lasting Power of Attorney, you are an administrator, not a guarantor. You are responsible for managing their funds, but the council cannot force you to spend your own money when addressing care home fees responsibility.

Legal Verification & Sources:

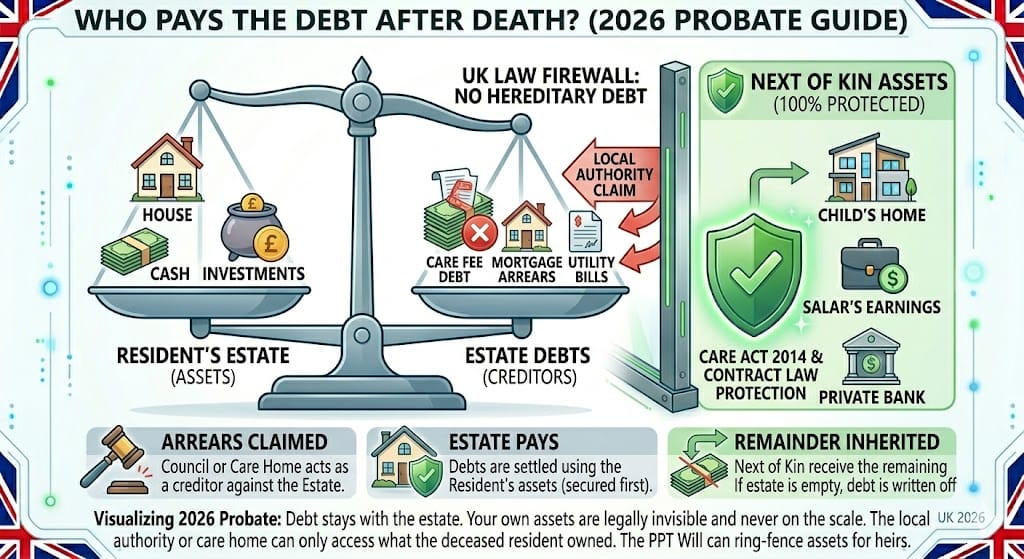

- Care Debt Recovery: Section 69, Care Act 2014 (Local Authority Powers).

- NHS Funding: National Framework for NHS CHC (2026 update).

- Property Trusts: Digital Assets (Property) Bill & Land Registry Guidance.

What the Council Cannot Assess:

- ✓ Child's Earnings: Your salary and workplace benefits are 100% exempt.

- ✓ Next of Kin's Property: Your own home is never part of their means test.

- ✓ Private Savings: Your personal bank accounts remain legally invisible.