Last updated: March 2026 — England & Wales Law | Author: Andrew Walters, Member of the Society of Will Writers

Property Protection Trust Wills: The Ultimate 2026 Homeowner's Guide

Everything you need to know about ring-fencing your home, protecting your children's inheritance, and navigating 2026 care cost laws.

What is a Property Protection Trust (PPT) Will?

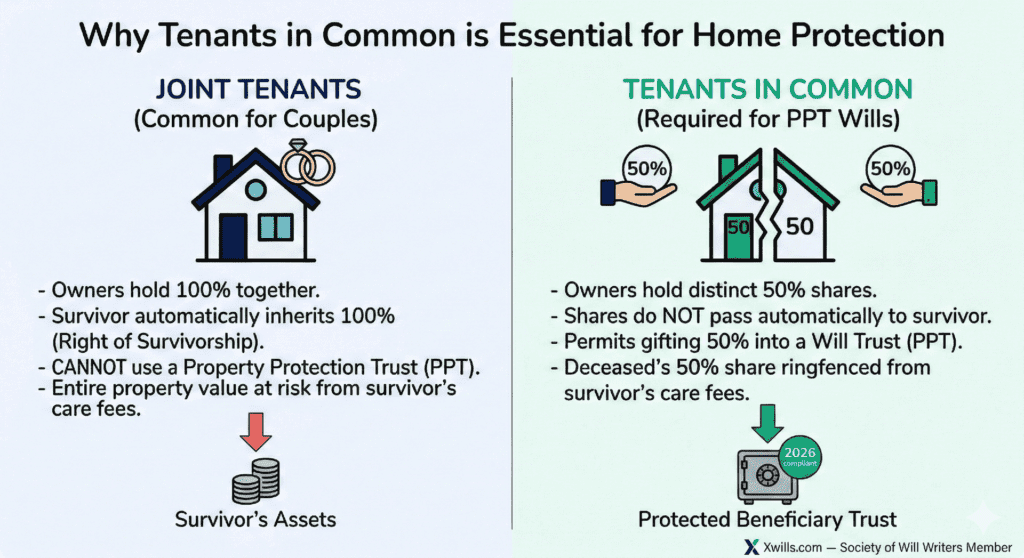

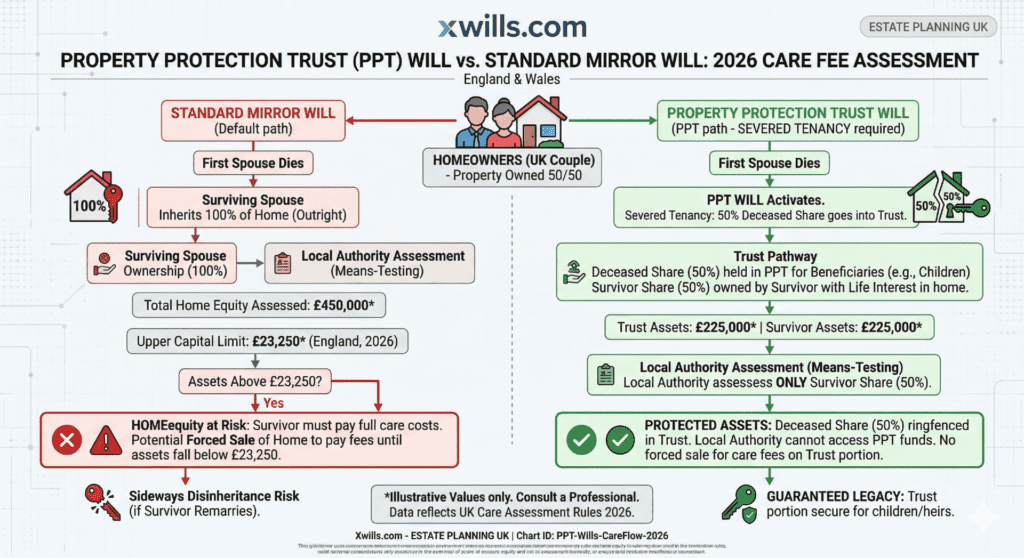

Direct Answer: A Property Protection Trust (PPT) Will is a specialised legal document that "splits" property ownership upon the first partner's death. It grants the survivor a "Life Interest" to stay in the home, while legally securing the deceased partner's 50% share for their children—protecting it from being consumed by care home fees or lost through remarriage.

In 2026, a PPT Will is considered the "gold standard" for homeowners. Unlike a standard Will, which leaves your assets "open" to future risks, a PPT Will is a specialised Trust designed to ring-fence your share of the family home.