- info@wills.com

- Address placeholder, Country

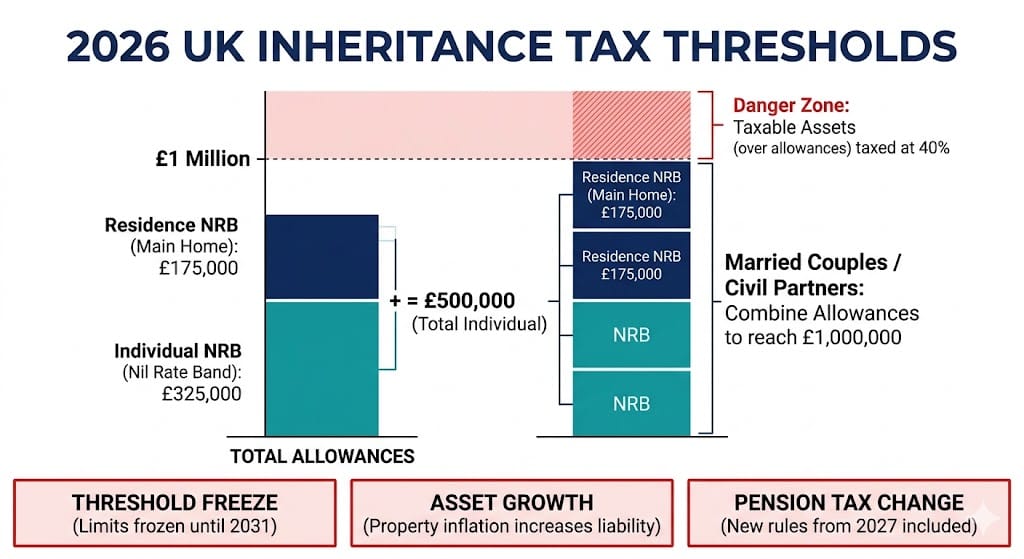

Regarding the question, "How Much is Inheritance Tax in 2026?"—most UK estates pay £0 if the total value is under £325,000. However, for homeowners leaving property to direct heirs, you can pass on up to £500,000 (individuals) or £1 Million (married couples) before the 40% tax rate applies. In 2026, the real risk is "Fiscal Drag," as frozen thresholds mean more families are being hit by tax bills as house prices rise.

Quick Answer: In 2026, the standard Inheritance Tax rate is 40%. However, most families utilise a combination of the Nil Rate Band (£325,000) and the Residence Nil Rate Band (£175,000) to create a tax-free threshold of £500,000 per person, or £1 Million per married couple. Understanding exactly how much is Inheritance Tax for your specific estate requires looking at the "Taper Cliff" and the downsizing rules.

HMRC does not tax the whole estate at once. To determine how much is Inheritance Tax, they apply allowances in this specific order:

The biggest mistake in 2026 planning is assuming the £1 Million exemption is guaranteed.

For estates valued over £2 Million, the RNRB is withdrawn at a rate of £1 for every £2 over the limit. In this "taper zone," every £100 you grow your wealth actually costs you £60 in eventual tax—40% headline rate plus the loss of 20% in allowances.

Case Example: An estate worth £2.35M loses the RNRB entirely. By using Business Property Relief (BPR) or Life Interest Trusts to keep the taxable estate below the £2M threshold, a family can save £140,000 in a single day.

If you are worried about how much is Inheritance Tax, leaving 10% of your net estate to charity triggers a legislated tax reduction. The 40% rate drops to 36% across the entire taxable remainder. This "socially conscious" planning often results in the heirs receiving a larger net sum than if no gift was made.

Our 2026 IHT Audit provides a precise calculation of your thresholds, tapers, and potential savings.

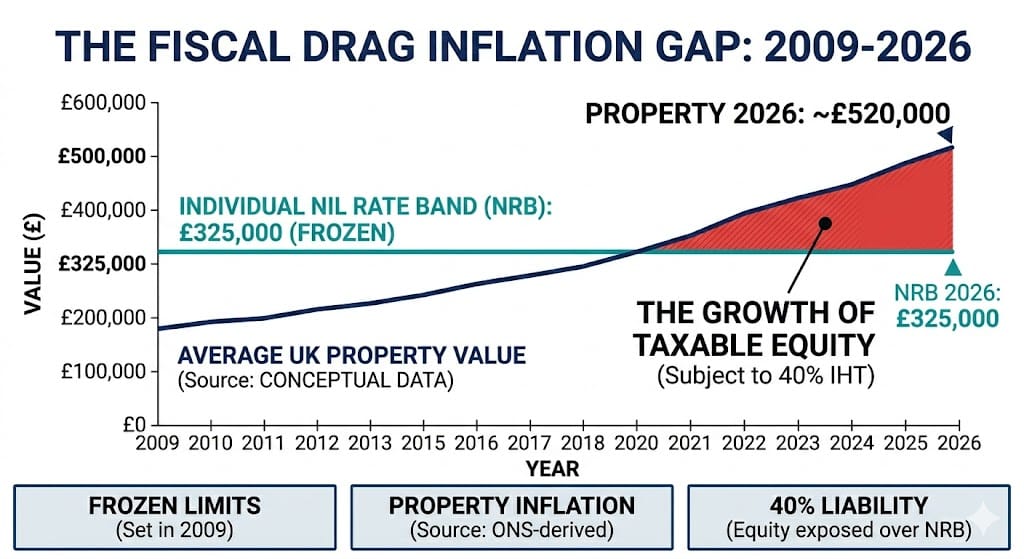

→ Get Your Bespoke 2026 AuditThe Short Answer: Even though the 40% rate hasn't changed, how much is Inheritance Tax in 2026 has increased because the tax-free thresholds have been frozen while property and asset values have soared. This "Fiscal Drag" quietly pulls thousands of modest family estates into the tax bracket every year.

The standard Nil Rate Band (£325,000) has been fixed since 2009. To maintain the same "purchasing power" and shield the same percentage of a family's wealth, that threshold should technically be over £520,000 today based on Consumer Price Index (CPI) data.

By maintaining the freeze until 2031, the government is executing a "stealth tax." As inflation devalues the pound, the real-terms value of your tax-free allowance shrinks, leaving a larger portion of your family home, savings, and investments exposed to the 40% HMRC charge.

This phenomenon creates a severe liquidity crisis for beneficiaries. Because IHT is calculated on the total estate value but must often be paid before Probate is granted, families find themselves with a massive cash liability tied up in a property they cannot yet sell.

The 2026 Liquidity Warning: In high-growth areas, "average" homes now routinely push estates past the £1 Million threshold. Because IHT must be settled before Probate is granted, many families face a "Cash Gap."

Without a Discretionary Trust Will to create deductible estate debts—or life insurance written in Trust to provide immediate liquidity—your heirs may be forced into high-interest "Probate Loans" just to satisfy HMRC before they can access the property's value.

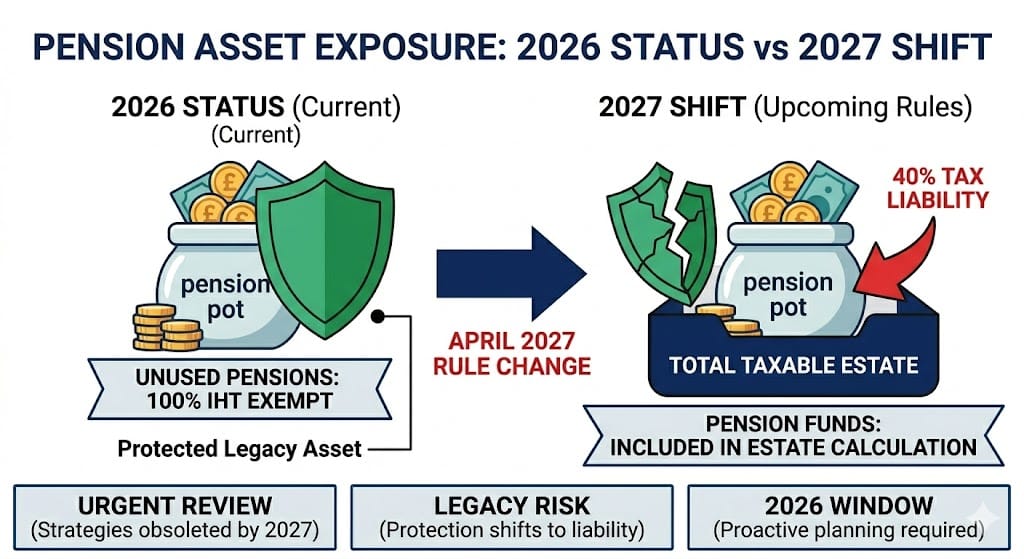

The Short Answer: Currently, in 2026, most unused pension pots remain exempt from Inheritance Tax. However, from April 2027, the UK government will bring unused pension funds into the value of your estate, exposing them to the 40% tax rate. This represents the most significant shift in how much is Inheritance Tax for the average family in decades.

The 2027 reform creates a complex tax trap. Not only will the pension pot be subject to 40% Inheritance Tax upon death, but if the deceased was over age 75, the beneficiary will also pay Income Tax at their marginal rate on any withdrawals.

Example: For a £100,000 pension pot left to a high-earning child, IHT takes £40,000. If the child then withdraws the remaining £60,000 as a 40% taxpayer, they lose another £24,000. The effective tax rate on that retirement legacy is a staggering 64%.

Historically, pensions bypassed probate because they were held "outside the estate" at the discretion of the pension trustees. With the 2027 inclusion, the simple nomination forms you signed years ago may now inadvertently trigger a massive tax bill. To protect the legacy, you must determine how much is Inheritance Tax based on your *total* asset pool, including SIPP and personal pension valuations.

The 2026 Strategy Window:

By reviewing your Trust structures and retirement drawdown strategy in 2026, you can potentially move funds or change your spending habits to reduce the estate's value before the 2027 "inclusion date." Waiting until the rules change could be an incredibly expensive mistake.

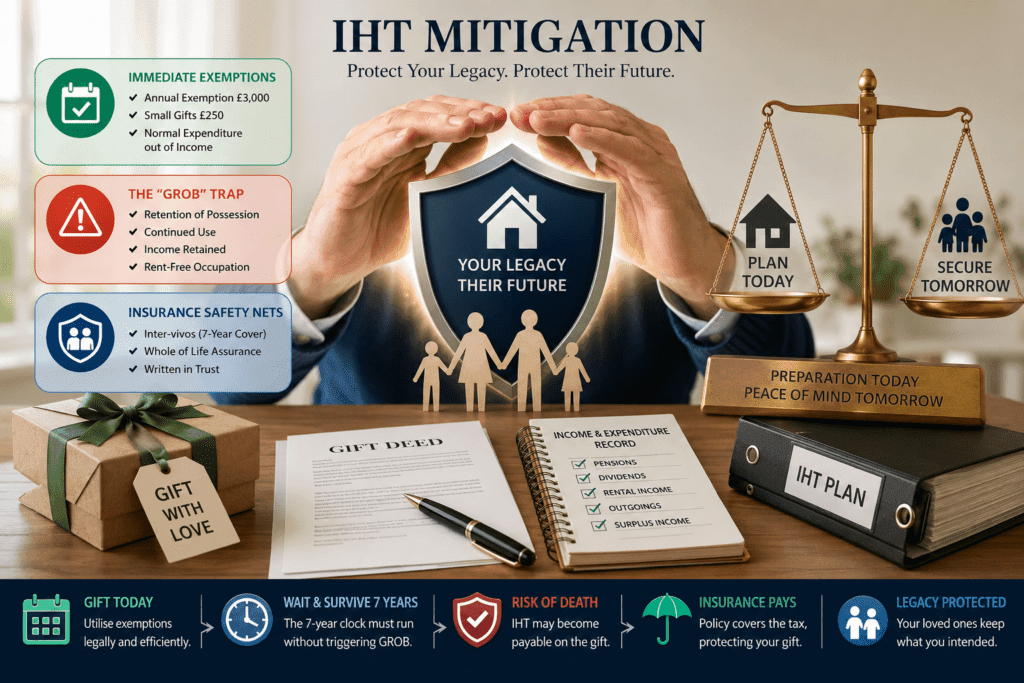

The Short Answer: You can reduce how much is Inheritance Tax by using immediate exemptions (like the £3,000 annual gift), making regular gifts from surplus income, or utilizing "Potentially Exempt Transfers" (PETs) which leave your estate entirely after seven years. For large, immediate gifts, many homeowners use Inter-vivos insurance to cover the tax risk during that 7-year window.

Certain gifts leave your estate instantly, meaning they do not count toward the calculation of how much is Inheritance Tax due on your death:

⚠️ THE COMPLIANCE BURDEN:

HMRC requires rigorous proof of "surplus." If you dip into capital or savings to fund these gifts, HMRC will reclassify them as taxable, drastically changing the math on how much is Inheritance Tax your family will eventually pay.

For gifts above your allowances (PETs), the 40% tax rate "tapers" down depending on how long you survive the gift. This is a critical factor in long-term wealth protection:

| Years between Gift & Death | Tax Rate on Gift |

|---|---|

| 0 – 3 Years | 40% |

| 3 – 4 Years | 32% |

| 4 – 5 Years | 24% |

| 5 – 6 Years | 16% |

| 6 – 7 Years | 8% |

| 7+ Years | 0% (Tax Free) |

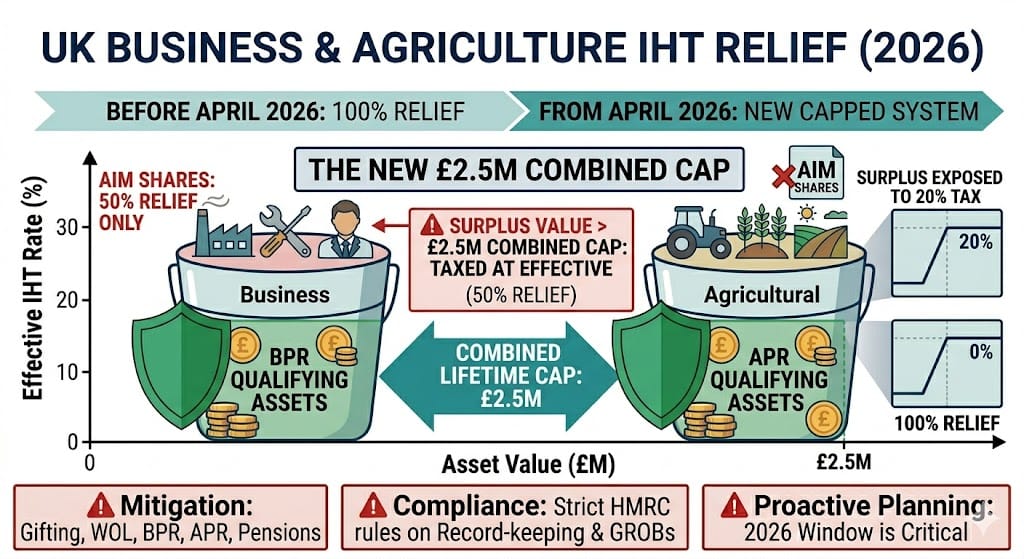

The Short Answer: As of 6 April 2026, 100% relief for business and agricultural assets is capped at a combined £2.5 Million per estate. For value exceeding this cap, relief is reduced to 50%, resulting in an effective tax rate of 20% on the surplus. Understanding how much is Inheritance Tax for business owners now requires calculating this tiered relief across trading assets and AIM portfolios.

The new cap applies to the aggregate value of all business (BPR) and agricultural (APR) assets. If your estate holds both, HMRC requires you to allocate the £2.5M allowance proportionally across those assets.

For married couples, the transferability of this allowance is the cornerstone of 2026 planning. By properly structuring Wills, a surviving spouse can utilize a combined £5 Million exemption. However, failing to use the first spouse's allowance at the point of death could lead to it being "swallowed up" by other assets, effectively wasting a £1 Million tax saving.

Under the new rules, value above the £2.5M cap receives 50% relief. Because the standard IHT rate is 40%, applying it to only half the value creates a 20% liability.

Mathematical Case Study (Family Farm/Business):

This creates a massive liquidity crisis. Without a Whole of Life insurance policy written in Trust, heirs may be forced to sell land or divest parts of the business to pay HMRC within the 6-month deadline.

The Short Answer: While homeowners often prioritize how much is Inheritance Tax, Social Care fees represent a more aggressive threat. While IHT is a one-time 40% charge on surplus wealth, care fees are an ongoing 100% liability that can consume nearly your entire estate, leaving only a statutory "safety net" of £23,250 in England or £50,000 in Wales.

In 2026, a common error is gifting assets to reduce how much is Inheritance Tax without considering local authority "look-back" powers. If a gift is deemed to have been made with the "significant expectation" of care needs, it is reclassified as Deliberate Deprivation of Assets.

Unlike the 7-year rule for IHT, there is no time limit for care fee assessments. A local authority can legally assess your finances as if you still owned a property transferred years prior, potentially leaving your family with a massive bill and no remaining assets to settle it.

| Liability Metric | Inheritance Tax (IHT) | Care Fees (England) | Care Fees (Wales) |

|---|---|---|---|

| Upper Capital Limit | £325k - £1m+ (Thresholds) | £23,250 | £50,000 |

| "Partial Funding" Zone | N/A | £14,250 - £23,250 | N/A (Full help below £50k) |

| The Family Home | RNRB Protection (£175k) | Exposed if living alone | Exposed if living alone |

| Gifting Constraints | 7-Year Rule (PETs) | No Statutory Time Limit | No Statutory Time Limit |

While care rules are aggressive, the Mandatory Property Disregard offers a vital shield. Your home is not counted in a financial assessment if it is still occupied by a spouse, a partner, or a relative over 60. By utilising Life Interest Trusts in 2026, you can "lock in" this protection for the surviving spouse while ensuring the capital is ultimately ring-fenced for your children—safe from both care fee erosion and the HMRC.

Related Guide: Are Next of Kin Responsible for Care Home Fees in 2026?

The 2026 landscape of frozen tax bands, pension reforms, and care fee liabilities is a minefield. Professional estate planning ensures your hard-earned assets go to your children, not the State.

Book Your Comprehensive 2026 Estate Review

0208 064 3806

info@xwills.com

Tilsop Farm,

Nash,

Ludlow,

Shropshire

SY8 3AX